Click here for Audio Version

Financial Markets- Stocks

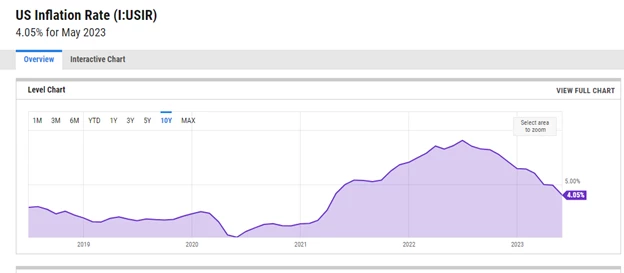

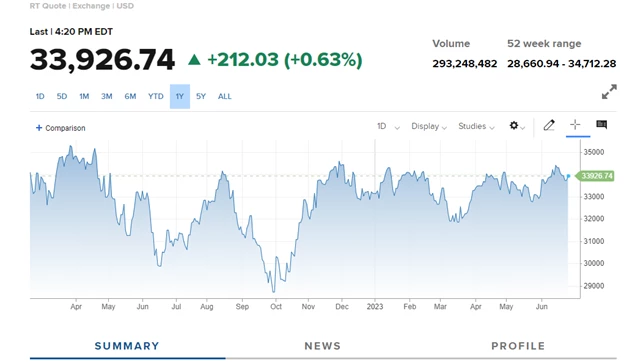

There appears to be some life in the stock market over the past 4 weeks. The Dow is now up roughly 1,200 pts since Memorial Day weekend, but still a little over 2,000 pts from its peak in December of 2021. Stable job reports and stable home price reports are beacons that the US economy could avoid a deep recession despite the Fed’s best efforts. To be clearer, the Fed’s primary objective is to bring inflation down to around 2%. At its peak inflation reached just over 9% in June of 2022. May’s inflation report reads just over 4%, so The Fed is about 75% of the way to its objective.

Financial Markets- Bonds (Mortgage Rates)

SO WHEN WILL MORTGAGE RATES START TO DROP??

There are 2 primary reasons to be confident that we can see mortgage rates in the 5’s in the near future.

1.) The spread between the 10 year US Treasury and the average 30 year fixed rate mortgage is historically wide by 1%. The last time the 10 Year US Treasury was around 3.8% you have to go back to around 2009. During that time the average 30 year fixed rate mortgage was around 5.4%. This places the gap between the two during that time at around 1.6%. While the gap between the 10 Year UST can certainly fluctuate, the average gap typically isn’t more than 2%. The current gap between the 10 Year US Treasury and the average 30 year fixed rate mortgage is currently 3.2%. This means that even if the 10 Year US Treasury doesn’t drop at all, if the gap moves to a more normal spread of 2%, we would see rates in the high 5’s.

2.) As mentioned above, inflation has now dropped from 9% to 4% in 1 year. As inflation continues to drop we will see a demand in US Bonds. Mortgage backed security yields will drop as demand for these bonds increase.

That didn’t answer the question of WHEN, but to quote a line from the movie Spaceballs, “When will then be now?...Soooon”. I will go out on a limb and say end of summer we will start to see progress in interest rates.

Currently mortgage backed securities have not quite fully recovered from when the bond market got spooked at the fears of the debt ceiling not getting raised in time. Since the 10 year US Treasury hasn’t been a great barometer of mortgage rates we will look at an actual mortgage backed security bond chart. To read this chart you want to remember that the price of the bond and the yield work in opposite directions. Meaning, when the price goes up, the yield, or our borrower’s interest rate, goes down. Here you can see that the price peaked at around mid Feb of 2023, which was when mortgage rates were at their lowest, where a 30 year fixed rate mortgage was hovering in the low 6’s. It almost got back there and stayed there a bit from March to middle of May, but the bottom fell out on fears the debt ceiling wouldn’t be raised in time to prevent defaults. There is about 175 basis points between its peak in price (or bottom in rate) and now. Remember that 100 basis points = about .25% in rate. So we are about ½ percent higher in rate today than we were in February of this year.

Southern Nevada Real Estate

The adjective that comes to mind to best describe the Southern Nevada real estate market, and for that matter most of the nation, is GRIDLOCK. While prices remain firm and in many markets starting to go back up the number of transactions are significantly lower. I researched the number of transactions for Southern Nevada over the past several years, and compared our last “normal” year, which I consider to be 2019 to this year. In 2019, just over 47,000 purchase transactions took place in Clark County. This is actually lower than the 3 years prior. We can toss out 2020 and 2021 fueled by the lowest interest rates ever. With May’s sales data in the books (3,818 total transactions) it brings the total number to 15,167 sales year to date for 2023. By the end of May 2019, there were 23,140 sales.

2023 is down 35% from the same time in 2019, which was one of the slowest sales paces in the past 10 years…

So how does the gridlock clear up? Lower mortgage rates will help. Folks that would like to move won't because they are not willing to trade a 3% mortgage for a 7% mortgage. If mortgage rates drop into low 5’s high 4’s, folks would be more willing to move because the specs of the new home that suits whatever reason they wanted to move won’t be nearly as expensive.

The other solution is simple but complex in how to implement the solution. More affordable housing…

Message me for free access to the following Realtor Tools! Take a look at Homebot! We can add your database to our Homebot account at no cost to you. Think of it like a 401k statement but for their home and it has over 80% open rate.